I found more and more media and analysts/brokers spurting a lot of garbage in this time of financial uncertainty. Well, maybe I am a little harsh, or probably I should just say that they need to go to their training again.

I suppose I have to realise that media make their money from a 'fantastic' breath taking stories and brokers make their money by encouraging frequent trades. But I have to say again for my peace of mind: Brokers or Stock Analyst recommendations and their price targets are useless! (Ok, I feel better now *smile*)

Another thing for us to put in our mind is that majority of analysts are highly compromise by the companies they cover, make them reluctant to report a 'sell' recommendation for fear of their access to the companies info and documents being revoked. It is said that 'hold' is a new 'sell', because the company will react badly if analysts produce sell recommendation.

We, as investors, have to realise that everyone has motivation when they're making recommendation, and part of our job is to determine or understand just what that motivation might be. Investor can listen, but we have to filter.

In Australia, the actions of financial analysts came under scrutiny after a Citigroup analyst downgraded the target share of Asciano from $6.08 to a meagre $0.82. This is the same analysts who had issued 20 reports of 'buy' recommendation before, with target price as high as $13.79a few months ago. How, why, had they have compromise before?

Another case worth mentioning is the one involved BrisConnections (please see my earlier post). Shares in the company slide rapidly from $1 on July IPO price to 0.1c, the lowest value a share can trade on the ASX. There are three analysts covering the company; Credit Suisse, JP Morgan, and Macquarie. In the week when BrisConnections fell to $0.05, those analyst posted target prices of $1.91, $2.10 and $0.93. What can we make of that? And of course the research houses claimed that they're completely independent of their broking arm.

So why we would read and listen to Broker or Analyst at all?

It's always a good thing to listen to any individual who have knowledge of a particular industry or company. It will increase our understanding of the business. But make sure you shield yourself from the 'buy/hold/sell' recommendation, or even from their number when they make their calculation. Instead, investor should get a good understanding of the long term picture of the company, their profitability and their position in the industry.

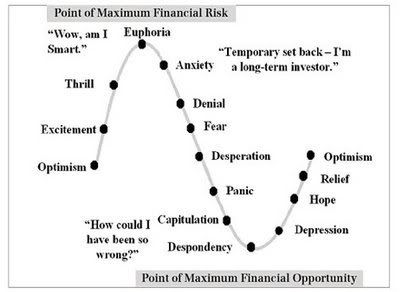

Tomas J. O'Loughlin, CFA, of Investment Portfolio Management, suggests that the best investment decisions in hard economic times are counterintuitive.

Tomas J. O'Loughlin, CFA, of Investment Portfolio Management, suggests that the best investment decisions in hard economic times are counterintuitive.